{kind=link}

Look, the tax code modified drastically proper underneath our noses. In case you are ready till April subsequent 12 months to begin excited about your taxes, you’re already giving the federal government manner an excessive amount of of your cash. With the sweeping updates from current legislative payments and new inflation-adjusted thresholds, the sport plan for the right way to scale back your tax invoice 2026 appears completely totally different than it did only a few years in the past.

You don’t should be a billionaire with offshore accounts to maintain extra of your paycheck. The tax code is principally an enormous rulebook that tells you precisely how the federal government desires you to spend, make investments, and save your cash. Whenever you comply with their guidelines, they reward you with large deductions and credit.

From large bumps in commonplace deductions to fully overhauled retirement catch-up guidelines, sensible monetary planning proper now will prevent hundreds of {dollars} later. Let’s stroll via ten extremely efficient, fully authorized methods you should use to scale back your tax invoice 2026 and shield your hard-earned wealth.

1. Maximize the New 2026 Retirement Account Limits

The simplest and most rapid technique to decrease your taxable earnings immediately is to cover your cash in a pre-tax retirement account. Each greenback you push into a conventional 401(okay) or conventional IRA is a greenback the IRS pretends you by no means made this 12 months. It’s the final word “pay your self first” technique that concurrently acts as a protect in opposition to federal earnings taxes.

|

2026 Retirement Plan |

Contribution Restrict |

Age 50+ Catch-Up |

Age 60-63 Tremendous Catch-Up |

|

401(okay), 403(b), 457 |

$24,500 |

$8,000 |

$11,250 |

|

Conventional & Roth IRA |

$7,500 |

$1,000 |

N/A |

|

SIMPLE IRA |

$16,500 |

$3,500 |

$5,250 |

Hit the New Base Limits First

Inflation changes simply bumped up how a lot you’ll be able to squirrel away. In 2026, you’ll be able to stash as much as $24,500 into your office 401(okay) or 403(b). If you happen to handle to max that out and occur to fall into the 24 % tax bracket, you immediately slash your tax invoice by practically six grand. That’s free cash staying in your pocket to compound over time fairly than funding authorities initiatives.

Past simply the tax financial savings, this cash will get put to work within the inventory market, constructing your long-term wealth. Even if you happen to don’t have entry to a office plan, funding a conventional IRA as much as the brand new $7,500 restrict offers you an instantaneous, dollar-for-dollar deduction, offered your earnings falls throughout the IRS pointers. You need to automate these contributions straight out of your paycheck so that you by no means even miss the cash.

Use the Age 60 to 63 Tremendous Catch-Up

Right here is the place the current retirement laws will get actually fascinating for older staff. If you happen to flip 60, 61, 62, or 63 at any level through the 2026 calendar 12 months, the federal government throws you an enormous lifeline known as the tremendous catch-up. As a substitute of the usual $8,000 catch-up allowed for anybody over 50, you get to pump an additional $11,250 into your 401(okay) fully tax-free.

Add that to the bottom restrict, and you’ll shelter $35,750 from taxes this 12 months alone. Oddly sufficient, when you hit your sixty fourth birthday, your restrict drops proper again right down to the usual catch-up stage. If you happen to sit on this particular candy spot, maxing this out is an absolute no-brainer to decrease your present tax burden whereas supercharging your nest egg proper earlier than retirement.

Typically the federal government takes away a tax break while you begin making an excessive amount of cash, they usually hardly ever warn you forward of time. This 12 months, excessive earners face a irritating new rule relating to their retirement catch-up contributions that requires an instantaneous shift in technique.

|

Earnings Degree in 2025 |

Age in 2026 |

Catch-Up Contribution Sort Allowed |

|

Below $150,000 |

50 or older |

Pre-Tax or Roth |

|

Over $150,000 |

50 or older |

Roth Solely (Necessary) |

The FICA Wage Threshold

Beginning in 2026, the foundations round catch-up contributions completely modified for upper-middle-class staff. If you happen to earned greater than $150,000 in FICA wages out of your present employer final 12 months, you’re formally locked out of constructing pre-tax catch-up contributions to your office plan. The IRS now strictly calls for that your $8,000 or $11,250 catch-up funds go straight into an after-tax Roth account.

As a result of Roth cash is taxed earlier than it goes in, you totally lose a really beneficial upfront tax deduction that you just most likely relied on closely in earlier years to convey down your adjusted gross earnings. This catches quite a lot of professionals fully off guard once they see their take-home pay shrink barely as a result of the tax deduction is gone.

Pivot Your Technique to Scale back Your Tax Invoice 2026

Shedding an $8,000 deduction hurts terribly if you happen to sit within the 32 or 35 % tax bracket. To offset this newly generated tax legal responsibility, you must look in all places else for obtainable tax shelters. You would possibly have to aggressively fund your Well being Financial savings Account, bunch your charitable donations, or notice some capital losses in your commonplace brokerage account.

Whereas paying taxes on the Roth catch-up stings a bit immediately, strive to have a look at the brilliant aspect. Do not forget that this Roth cash will develop totally tax-free for the remainder of your life. It received’t be topic to Required Minimal Distributions (RMDs), which provides you unbelievable flexibility and defensive energy in opposition to taxes later in retirement.

3. Exploit the Upgraded Well being Financial savings Account (HSA)

When you’ve got a Excessive Deductible Well being Plan (HDHP), ignoring your Well being Financial savings Account is principally a monetary tragedy. It stays the best possible tax-advantaged account obtainable to working People, and the funding limits simply went up once more this 12 months.

|

2026 HSA Protection Sort |

Contribution Restrict |

Age 55+ Catch-Up |

Tax Deduction Standing |

|

Particular person |

$4,400 |

$1,000 |

100% Pre-Tax |

|

Household |

$8,750 |

$1,000 |

100% Pre-Tax |

Perceive the Triple Tax Benefit

An HSA beats a typical 401(okay) and a Roth IRA mixed, fingers down. First, the cash goes into the account totally tax-free, which lowers your taxable earnings proper now on a dollar-for-dollar foundation. Second, you don’t simply go away it in money; you’ll be able to truly make investments the funds in index funds or ETFs, and the cash grows fully tax-free.

Third, so long as you utilize the cash to pay for certified medical bills, the withdrawals are totally tax-free. You by no means pay a single dime of federal earnings tax on that cash if you happen to play strictly by the foundations. It’s the solely account in your complete US tax code that provides this highly effective triple tax benefit, making it a compulsory software for wealth constructing.

Pay Money Now and Preserve the Receipts

To essentially hack the system and maximize your wealth, totally fund your HSA to the $8,750 household restrict however don’t spend a penny of it in your present copays or prescriptions. As a substitute, pay in your minor medical payments proper out of your common checking account. Let the HSA cash sit invested within the inventory market so it may compound over a decade or two.

The IRS at present has completely no time restrict on while you reimburse your self for medical prices. Preserve your digital receipts organized in a cloud folder. Twenty years from now, you’ll be able to money out these previous receipts and pull out large chunks of tax-free cash to fund your retirement life-style.

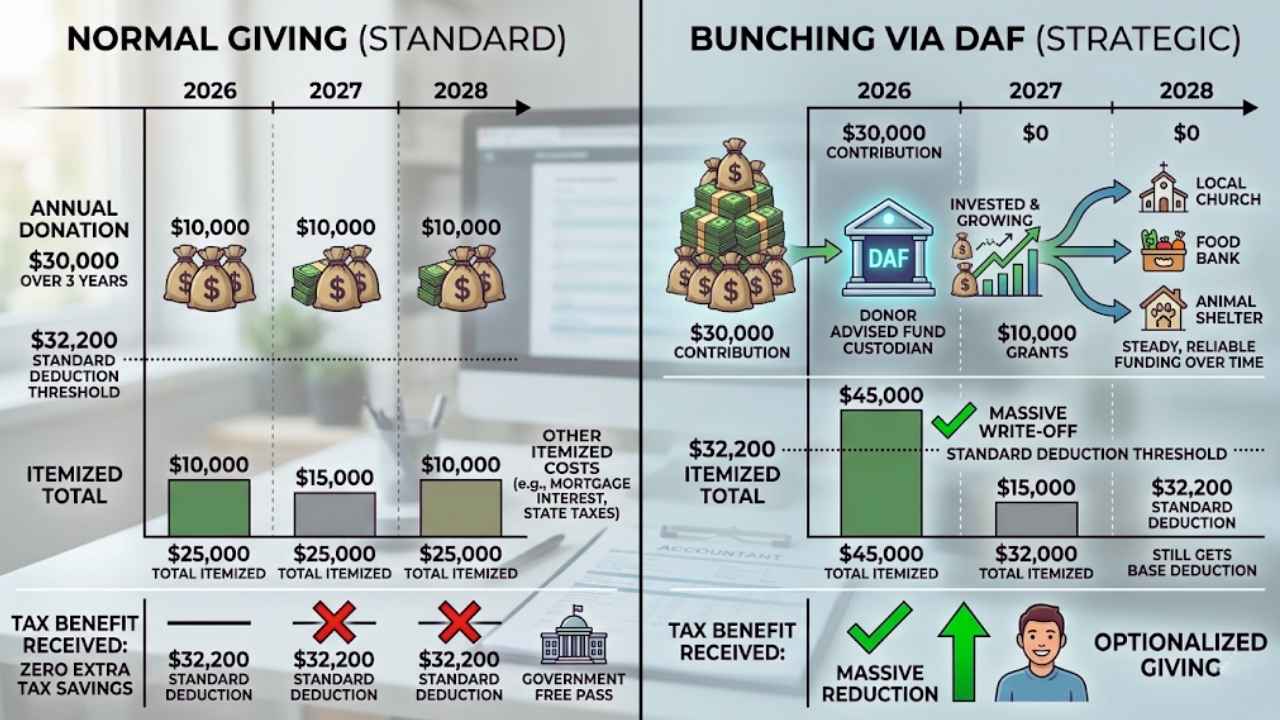

4. Bunch Your Charitable Giving with a DAF

The up to date commonplace deduction is extremely beneficiant proper now. In 2026, a married couple will get an enormous $32,200 commonplace deduction proper off the bat. The issue is that until your itemized deductions like mortgage curiosity, state taxes, and charity exceed that massive quantity, giving cash to your favourite trigger does completely nothing to decrease your taxes.

|

Giving Technique |

Annual Donation |

2026 Complete Deduction Claimed |

Tax Profit Obtained |

|

Regular Giving (Normal) |

$10,000/12 months for 3 years |

$32,200 (Normal Deduction) |

Zero further tax financial savings |

|

Bunching by way of DAF |

$30,000 in Yr 1 |

$30,000 + different itemized prices |

Large discount in Yr 1 |

|

Normal in Years 2 & 3 |

$0 |

$32,200 (Normal Deduction) |

Nonetheless will get base deduction |

Beat the Normal Deduction Threshold

If you happen to usually give ten thousand {dollars} a 12 months to your native church, meals financial institution, or animal shelter, you doubtless simply take the usual deduction each single 12 months and get zero tax reward in your ongoing generosity. The federal government is principally getting a free move whilst you fund these organizations.

The extremely sensible workaround is a technique known as bunching. As a substitute of giving a bit of bit yearly, you cram three or 4 years’ price of charitable donations right into a single calendar 12 months to pressure your self over the excessive hurdle of the usual deduction.

Open a Donor Suggested Fund

You execute this technique easily by opening a Donor Suggested Fund (DAF). You dump thirty thousand {dollars} into the fund in 2026. This single, large contribution pushes your complete itemized deductions well past the $32,200 threshold, permitting you to safe an enormous tax write-off this 12 months.

The money sits safely within the DAF, the place it may be invested and develop, and also you merely instruct the fund supervisor to distribute the cash to your chosen charities regularly over the subsequent three years. You get an enormous tax break immediately, the charities get their regular, dependable funding over time, and also you seamlessly optimize your giving.

5. Roll Unused 529 Faculty Funds right into a Roth IRA

For the longest time, mother and father have been afraid of overfunding a 529 school financial savings plan. In case your child obtained a full-ride scholarship or determined to change into a plumber as an alternative of going to a four-year college, taking that cash out triggered nasty penalties and taxes on the expansion. The foundations have lastly shifted closely in favor of the mother and father.

|

529 Rollover Rule |

Requirement |

Limitation |

|

Account Age |

Have to be open 15+ years |

Can’t bypass this rule |

|

Contribution Timing |

Contributions in final 5 years ineligible |

Solely older funds can transfer |

|

Annual Switch Restrict |

Matches Roth IRA restrict ($7,500 in 2026) |

Have to be finished over a number of years |

|

Lifetime Cap |

Most of $35,000 per beneficiary |

Exhausting ceiling |

Jumpstart Your Child’s Retirement

When you’ve got leftover cash sitting in a 529 plan that has been open for at the least fifteen years, now you can roll these funds instantly right into a Roth IRA for the very same account beneficiary. This implies you’ll be able to confidently front-load these training accounts when your children are younger with out the extraordinary worry of getting penalized later.

You get the state tax deduction on the entrance finish in lots of states, and in the event that they don’t use all the cash for tuition or books, you’ll be able to magically convert it right into a tax-free retirement nest egg for them. It fully adjustments the chance profile of faculty financial savings.

Thoughts the Strict Guardrails

The IRS undoubtedly didn’t make this a complete free-for-all, so you must comply with the playbook carefully. You’ll be able to solely roll over an quantity equal to the annual Roth IRA contribution restrict, which sits at $7,500 for 2026. When you’ve got $30,000 leftover within the account, it’s going to take you 4 full years to maneuver all the cash over safely.

Additionally, any contributions or earnings made within the final 5 years are strictly off-limits for this switch. Regardless of the bureaucratic pink tape, this can be a phenomenal wealth switch software that secures your little one’s monetary future whereas dodging steep penalty taxes.

6. Maximize 100 % Bonus Depreciation for Enterprise

If you happen to personal a small enterprise or work as a freelancer, 2026 is an absolute goldmine. Because of provisions completely enacted not too long ago, the flexibility to write down off massive gear purchases and protect your money circulation from the federal government is best than it has been in years.

|

Asset Sort |

Earlier Depreciation Rule |

2026 Bonus Depreciation Rule |

|

Heavy Autos (over 6,000 lbs) |

Phasing down (20%) |

100% Yr One Deduction |

|

Equipment & Gear |

Phasing down (20%) |

100% Yr One Deduction |

|

Certified Enchancment Property |

15-year straight line |

100% Yr One Deduction |

Purchase Gear and Slash Your Income

Usually, while you purchase a forty-thousand-dollar industrial van or heavy manufacturing equipment, the IRS forces you to write down off that expense slowly over a torturous 5 or ten years. That doesn’t provide help to in any respect if you’re staring down an enormous tax invoice immediately and want rapid reduction.

Below the at present lively guidelines, companies can take one hundred pc bonus depreciation on qualifying belongings positioned into service this 12 months. This implies you’re taking your complete deduction instantly in opposition to your 2026 income, quickly bringing your taxable revenue right down to a way more manageable stage.

Renovate Your Business Area

It truly will get even higher for brick-and-mortar house owners. Certified Enchancment Property now formally qualifies for this rapid write-off provision. If you happen to personal a restaurant, a dental apply, or a retail store and also you drop 200 thousand {dollars} renovating the inside to make it look fashionable, you’ll be able to deduct your complete price in opposition to your present 12 months income.

If you happen to had a blowout 12 months in gross sales and have to dramatically shelter that money circulation from the IRS, upgrading your gear or reworking your area earlier than December 31 is the final word, completely authorized tax protect.

7. Clear Up Your Portfolio with Tax Loss Harvesting

Investing exterior of a retirement account means you finally should pay capital features taxes when issues go nicely. However sensible traders by no means, ever pay taxes on their successful shares with out first checking to see if they’ll offset the invoice with their shedding shares.

|

Transaction Sort |

Monetary Affect |

Tax Lead to 2026 |

|

Promote Inventory A |

$10,000 Revenue |

Owe capital features tax |

|

Promote Inventory B |

$10,000 Loss |

Generates a tax deduction |

|

Internet Affect |

$0 Acquire |

Zero taxes owed |

|

Promote Inventory C |

Extra $3,000 Loss |

Deduct in opposition to W-2 strange earnings |

Cancel Out Your Capital Good points

Tax loss harvesting is a basic technique it’s best to run each single December earlier than the 12 months closes. If you happen to offered a mutual fund in June and made ten thousand {dollars}, you owe heavy taxes on that realized revenue.

Nevertheless, if you happen to look carefully at your portfolio and spot one other inventory or fund is sitting deep within the pink, you’ll be able to deliberately promote it at a ten thousand greenback loss. These two particular transactions fully cancel one another out in your tax return, appearing as an ideal counterbalance to erase the tax legal responsibility totally.

Erase Your Strange Earnings

If you happen to had a horrible, risky 12 months within the inventory market and your losses far exceed your features, the IRS truly throws you a small bone. You’ll be able to take as much as $3,000 of these extra inventory market losses and use them to decrease your strange earnings, corresponding to your W-2 wage. Something past that $3,000 restrict merely will get carried ahead to subsequent 12 months, indefinitely.

You simply should be careful for the difficult wash sale rule. You’ll be able to’t promote a shedding inventory and purchase the very same inventory again the subsequent day simply to get the tax break. You will need to wait thirty-one days or purchase a very totally different ETF that tracks an analogous index to remain invested.

8. Grasp the New 1099-Okay Reporting Guidelines

When you’ve got a aspect hustle, promote classic objects on eBay, or freelance and receives a commission via third-party platforms like PayPal or Venmo, the IRS monitoring guidelines have flipped forwards and backwards endlessly. For 2026, the mud has lastly settled, and it’s worthwhile to know precisely what paperwork is coming your manner.

|

Fee Processor Sort |

2026 Reporting Threshold |

Type Issued |

|

Third-Occasion (PayPal, Venmo) |

$20,000 AND 200 transactions |

1099-Okay |

|

Credit score Card Processors |

Any quantity ($0.01+) |

1099-Okay |

|

Direct Shopper Funds |

$2,000+ |

1099-NEC |

Separate Private and Enterprise Accounts

The present standing rule states that third-party platforms solely should ship you a 1099-Okay tax doc if you happen to cross $20,000 in income and have greater than 200 particular person transactions. Nevertheless, if you happen to combine your private and enterprise cash in the identical app, issues get extremely messy quick.

In case your roommate sends you half the lease cash on Venmo and it by chance pushes you over the reporting restrict, the IRS assumes all of it’s taxable enterprise earnings. Absolutely the best technique to shield your self and preserve your sanity is to open a very separate digital pockets or checking account completely in your aspect hustle.

Monitor Each Single Expense

Receiving a 1099-Okay doesn’t imply you mechanically owe taxes on that enormous gross quantity printed on the web page. You solely ever pay taxes in your precise web revenue. You must begin treating your small aspect hustle like an actual, respectable company.

Monitor the price of the products you offered, the cardboard delivery supplies, the steep platform charges, and even the portion of your property web you utilize to run your digital store. Deducting all these respectable bills meticulously is precisely the way you scale back your tax invoice 2026 when the IRS wrongly assumes you made an enormous fortune promoting crafts on-line.

9. Put Your Kids on the Household Payroll

If you happen to function a sole proprietorship, an LLC, or a partnership, hiring your children is a totally authorized, extremely inspired wealth switch technique that primarily creates tax-free cash in your complete household unit.

|

Household Member |

2026 Normal Deduction |

Federal Earnings Tax Charge |

Enterprise Deduction Standing |

|

Single Youngster (W-2 Worker) |

$16,100 |

0% as much as deduction restrict |

100% Deductible for Enterprise |

Shift Earnings to a Zero % Bracket

The underlying math right here is totally good for enterprise house owners. You might be doubtless sitting in a excessive tax bracket, most likely paying 24 or 32 % on your small business earnings. Your little one, nevertheless, is sitting in a zero % tax bracket. In 2026, a single filer will get a $16,100 commonplace deduction.

If you happen to rent your teenage child to run your organization’s social media accounts, sweep the warehouse flooring, or file digital paperwork, you’ll be able to legally pay them as much as $16,100 this 12 months. Due to their commonplace deduction, they pay completely zero federal earnings tax on that cash.

Create a Generational Wealth Machine

In the meantime, your small business will get to write down off their complete $16,100 wage as a typical, totally deductible enterprise expense. This drastically lowers your taxable revenue and slashes your individual steep tax invoice. The work must be actual, age-appropriate, and paid at a standard, justifiable market fee—you’ll be able to’t pay a toddler fifty bucks an hour to staple papers.

As soon as they’ve that earned earnings sitting of their checking account, they’ll take $7,500 of it and drop it straight right into a Roth IRA. You simply systematically lowered your taxes and primarily made your teenager a future millionaire by the point they hit retirement age.

10. Set up Inexperienced Vitality Upgrades Earlier than Credit Sundown

The federal government deeply likes to subsidize residential vitality effectivity, however the clock is ticking loudly on a number of the finest tax credit obtainable to American householders. Bear in mind, a tax credit score is exponentially higher than a typical tax deduction. A deduction simply lowers your taxable earnings, however a credit score is a straight dollar-for-dollar discount of the particular tax you owe the IRS.

|

Inexperienced Dwelling Improve |

Tax Credit score Sort |

Max Annual Restrict |

|

Vitality Environment friendly Home windows/Doorways |

25C Credit score (30% of price) |

$1,200 combination restrict |

|

Warmth Pumps / Biomass Stoves |

25C Credit score (30% of price) |

$2,000 separate restrict |

|

Photo voltaic Panels / Battery Storage |

25D Credit score (30% of price) |

No higher greenback restrict |

Declare the 25C and 25D Credit

If your property’s HVAC system is on its final legs, 2026 is the right 12 months to interchange it with a contemporary, high-efficiency warmth pump. You’ll be able to simply seize a tax credit score of as much as $2,000 only for making the environmentally pleasant change. In case you are changing drafty exterior doorways, previous home windows, or including heavy insulation to your attic, you’ll be able to declare as much as $1,200 yearly.

As a result of the 25C credit score resets each single 12 months, sensible householders unfold their renovations out strategically. Do the home windows this 12 months, do the doorways subsequent 12 months, and declare the utmost credit score each instances to squeeze each dime out of this system.

Go Massive with Photo voltaic Initiatives

In case you are planning main structural additions like rooftop photo voltaic panels or residential battery storage methods, the 25D Residential Clear Vitality Credit score nonetheless gives an enormous 30 % credit score with no higher cap in any respect. Drop thirty grand on an enormous photo voltaic array, and also you wipe 9 thousand {dollars} straight off your federal tax invoice immediately.

These particular residential credit are slowly pacing towards expiration later this decade, making rapid motion extremely profitable for householders wanting to scale back their tax invoice 2026 and decrease their month-to-month utility prices.

Closing Ideas

The tax code shifted massively underneath current laws, and burying your head within the sand will completely price you cash you’ll be able to’t afford to lose. The methods are laid out proper in entrance of you, ready to be executed. By maximizing your tremendous catch-up contributions, funneling money via a triple-tax-advantaged HSA, front-loading enterprise gear purchases, and retaining your aspect hustle bills completely documented, you’ll be able to legally drain the water out of your taxable earnings pool.

If you wish to efficiently scale back your tax invoice 2026, you must cease appearing like tax season occurs solely in April. Tax season occurs each single time you get a paycheck, purchase a enterprise asset, or make an funding. Take management of your numbers immediately, seek the advice of with a certified CPA to map out your particular brackets, and preserve your wealth proper the place it belongs.

Often Requested Questions (FAQs) About Scale back Tax Invoice Legally

What’s the new commonplace deduction for 2026?

Because of inflation and new laws, the usual deduction jumped considerably. Single filers can declare $16,100, heads of family get $24,150, and married {couples} submitting collectively can declare an enormous $32,200. This makes itemizing pointless for the overwhelming majority of taxpayers.

Can I nonetheless deduct my state and native taxes (SALT) in 2026?

Sure. If you happen to select to itemize fairly than take the usual deduction, the SALT cap restrict has been adjusted to $40,400 for joint filers and $20,200 for married {couples} submitting individually. This can be a momentary enhance that gives large reduction in high-tax states.

What’s the SECURE 2.0 tremendous catch-up rule?

In case you are between the ages of 60 and 63 through the 2026 calendar 12 months, you’re allowed to make an elevated catch-up contribution of $11,250 to your office 401(okay), completely changing the usual $8,000 restrict allowed for different staff over 50.

Why did I obtain a 1099-Okay from Venmo for my private transactions?

If you happen to combine enterprise and private funds in a single digital account and cross $20,000 and 200 transactions, the platform reviews the gross quantity to the IRS. You will need to fastidiously doc and separate private reimbursements (like splitting dinner) from taxable enterprise income in your precise tax return.

Can I declare one hundred pc bonus depreciation on used gear?

Sure, completely. The up to date guidelines completely restored one hundred pc bonus depreciation for qualifying belongings. The gear could be calmly used, offered it’s completely new to you and you bought it from an unrelated get together through the lively calendar 12 months.

How do I keep away from the kiddie tax when hiring my youngsters?

The “kiddie tax” usually applies to unearned earnings, like large dividends or capital features on investments in a baby’s identify. Whenever you put your little one on the precise payroll with a W-2 for respectable work, that’s earned earnings, which is sheltered as much as their commonplace deduction of $16,100 with out triggering the kiddie tax.