{kind=link}

Key Messages

- Companies that legally require a medical director usually face SBA eligibility points if that particular person is handled as a key administration worker.

- The SBA might require key managers to personally assure a mortgage, even when they personal 0 % of the enterprise.

- Third-party medical administrators or MSA buildings can scale back this threat by making medical oversight replaceable.

- CDC Small Enterprise Finance lends nationwide to med spas, IV hydration clinics, and wellness companies with compliant buildings.

- The sooner a enterprise opinions their construction with a lender, the simpler the SBA mortgage course of turns into.

When opening a med spa, IV hydration clinic, well being middle, weight-loss observe, or different wellness enterprise, medical oversight is commonly a authorized requirement. In lots of states, these companies can’t even get off the bottom with no medical director or supervising doctor on board.

The difficult half for founders often comes when this requirement bumps up towards SBA mortgage medical director guidelines.

At CDC Small Enterprise Finance, a part of the Momentus Capital branded household of organizations, we frequently speak to debtors, a lot of whom are nurses, registered nurses (RNs), or nurse practitioners (NPs), who’re caught off guard to search out that their SBA utility has stalled not due to credit score, money movement, or expertise, however as a result of the medical director is considered as a key administration worker who isn’t keen to ensure the mortgage. This is without doubt one of the commonest points CDC mortgage officers come throughout, particularly with start-ups that have already got contracts in place. As Stacey Sanchez defined, “That is the most important ache level we see. They name us, they’ve all of the stuff lined up however want financing. Then they notice too late how the medical director is considered by the SBA.”

The silver lining? With the appropriate set-up, many of those companies can really qualify for SBA 7(a) Neighborhood Benefit loans.

Does Your Enterprise Want a Medical Director?

Whether or not or not a enterprise wants a medical director actually depends upon the state legal guidelines and the providers supplied. A medical director is a licensed doctor who oversees the medical aspect of a healthcare or wellness observe to assist guarantee providers are delivered safely and meet medical requirements.

Whereas they is probably not concerned in delivering providers or operating the enterprise, the medical director gives required doctor oversight, establishes medical protocols, and helps hold the enterprise compliant with state legal guidelines and rules. If a clinic gives medical providers, particularly people who contain prescriptions or medical procedures, most states would require a medical director.

This comes up incessantly in SBA functions for med spas and wellness clinics. Megan Stuit, a CDC Small Enterprise Finance mortgage officer who opinions these offers practically each different week, usually has to stroll debtors by way of the medical director necessities early within the course of. “The difficulty is {that a} nurse or different practitioner can present the service, however the state nonetheless desires a medical director overseeing the operation, despite the fact that the medical director actually doesn’t do any of the providers.”

Frequent Companies that Require a Medical Director

- Medical spas and aesthetic clinics

- IV hydration and wellness infusion clinics

- Weight-loss clinics utilizing prescription drugs

- Well being facilities not owned by a doctor

- Nurse-owned or NP-led regulated wellness companies

As soon as it’s decided {that a} medical director is important, the SBA desires to know if that enterprise is reliant on one particular doctor to function.

What the SBA Seems at When a Enterprise Wants a Medical Director

When lenders are taking a look at SBA 7(a) Neighborhood Benefit loans for regulated wellness companies, they focus much less on the precise title of a job and extra on whether or not the enterprise can function with out that individual. They’re additionally taken with who has the ultimate say on necessary selections. From the SBA’s standpoint, any individual {that a} enterprise can’t legally perform with out is necessary.

If a clinic wants a medical director to function, SBA lenders might view that particular person as a key administration worker. Below SBA guidelines, key managers usually need to personally assure the mortgage, even when they don’t personal the enterprise. This implies lenders should decide if the enterprise is closely depending on one individual.

Many wellness companies are unclear in how SBA underwriting evaluates roles tied to required medical oversight. Below SBA pointers, people who both personal 20 % or extra of the enterprise or are thought of key administration workers are required to ensure the mortgage. As Stacey Sanchez defined throughout a current assessment of those eventualities, “That key administration worker piece is the road that catches them. The medical administrators aren’t house owners. But when they’re thought of a key administration worker, and that medical director doesn’t wish to be liable for the mortgage, the enterprise doesn’t qualify.”

Key Inquiries to Assume About Normally Embrace:

- Is a medical director required by state regulation?

- Is the enterprise reliant on a selected doctor to perform?

- Who makes the day-to-day enterprise selections?

- Who oversees the medical aspect versus the executive aspect?

Many debtors suppose that because the medical director is merely a licensing formality, it received’t influence the underwriting course of. Nonetheless, lenders must assess if the enterprise can legally and virtually hold operating if that individual had been to depart. That is usually found later than it needs to be. As Megan famous, “Oftentimes, it’s too far alongside by the point they ask the query. They have already got the physician in place, and now we’re making an attempt to work backward.”

If the enterprise can’t function legally with out that one physician, and that physician isn’t keen to again the mortgage, it may well jeopardize eligibility, turning what might have been a manageable problem right into a irritating delay or perhaps a denial.

Already working with a third-party medical director firm?

See how a lot you might qualify for with an SBA 7(a) Neighborhood Benefit mortgage.

How Third-Celebration Medical Director & MSA/MSO Fashions Assist

That is the place third-party medical director corporations, together with Administration Companies Settlement (MSA) or Administration Companies Group (MSO) buildings, actually come into play.

An MSA is a contract utilized by nurse-owned and non-physician-owned medical spas, IV hydration clinics, and different regulated wellness companies to assist meet state licensing and medical oversight necessities, with out giving possession to a doctor. The MSO acts because the behind-the-scenes working firm.

On this set-up, the borrower is the MSO and manages the clinic each day. This contains the whole lot from operations and staffing to scheduling, affected person expertise, billing, advertising and marketing, services, and general enterprise technique. The house owners are usually nurses, nurse practitioners, or different well being care professionals who’re certified to run the enterprise however, in keeping with state regulation, want a doctor concerned for medical oversight.

From a lending perspective, this will considerably alter the underwriting course of as a result of the medical director function turns into extra interchangeable, even whereas medical oversight stays intact. Nicely-structured MSAs allow med spas to perform effectively, permitting the MSO to focus on enterprise progress whereas the third-party medical director firm ensures compliance and medical oversight.

These buildings are likely to work finest when they’re arrange early and reviewed with each licensing and lending in thoughts. As Stacey defined, “Thus far, these MSAs, third-party contracts, aren’t required to be accredited by the SBA. That flexibility makes a distinction after we’re reviewing the construction.”

This distinction usually permits lenders to focus on the enterprise fundamentals quite than getting caught on one particular person’s willingness to ensure the mortgage.

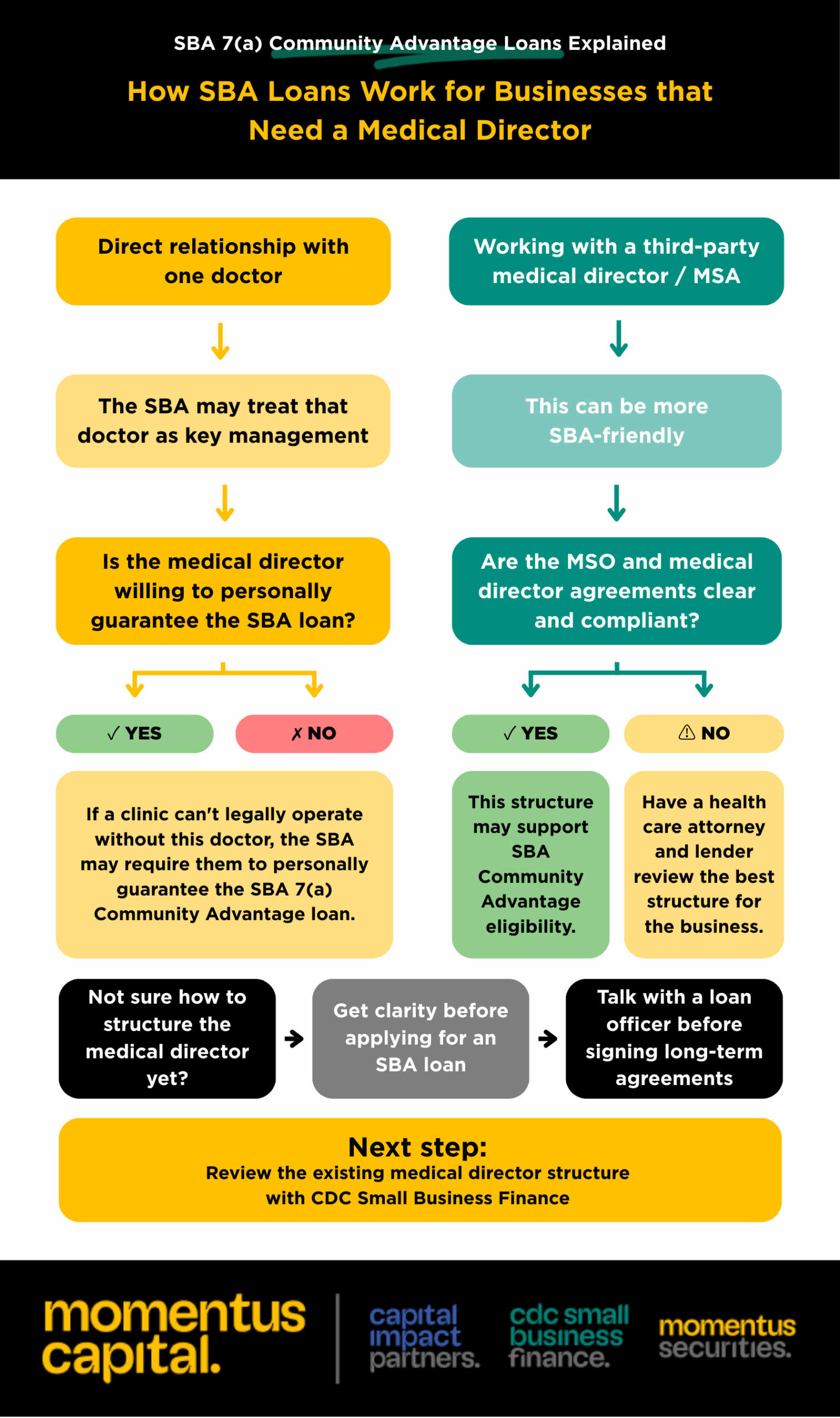

Right here’s a helpful flowchart that outlines the important thing determination factors lenders think about when taking a look at SBA 7(a) Neighborhood Benefit loans for companies needing a medical director. It captures the frequent eventualities mortgage officers encounter, like direct contracts with particular person physicians, third-party medical director corporations, and MSO buildings. Plus, it factors out the place eligibility points usually pop up.

If a med spa or wellness middle remains to be determining find out how to arrange their enterprise, this software can present steerage on when it’s sensible to hit pause and seek the advice of with a lender earlier than locking into long-term agreements, quite than operating into issues after submitting mortgage functions.

Earlier than You Apply: Guidelines for SBA-Prepared Medical Director Constructions

Earlier than making use of for an SBA 7(a) Neighborhood Benefit mortgage, it’s a good suggestion to place the enterprise construction to the take a look at, identical to a lender would.

Debtors who navigate the underwriting course of easily usually have a transparent understanding of whether or not a medical director is legally needed, how that function is ready up, and who has the ultimate say in enterprise operations. Mortgage officers constantly stress that having readability from the beginning is extra necessary than having the whole lot completely documented on day one.

That’s why taking a detailed have a look at the med spa or wellness middle’s construction early on can save a whole lot of time down the street, particularly if it’s a start-up nonetheless understanding contracts.

Earlier than making use of for an SBA 7(a) Neighborhood Benefit mortgage, be sure that the reply is a assured “sure” to many of the following:

- The state’s authorized requirement for a medical director is known.

- The medical director relationship is documented and compliant.

- Possession and management are clearly outlined.

- MSA or medical director agreements have been reviewed by an legal professional who routinely handles company observe of drugs (CPOM) buildings.

- The enterprise construction has been mentioned with a lender earlier than submitting an utility.

Doing this groundwork can save months of delays and even assist keep away from having an SBA mortgage declined.

When to Speak to a Lender If a Enterprise Wants a Medical Director

The most effective time to speak with a lender is earlier than the medical director or MSA agreements are finalized.

As soon as these contracts are signed, making modifications can result in further authorized work and delays. Mortgage officers usually encounter debtors who need to restructure their agreements just because the preliminary contract didn’t meet SBA necessities. Timing is commonly the deciding issue. As Stacey defined, “If we see it early, we are able to often information companies. As soon as agreements are signed, that’s when it will get onerous.”

For wellness companies which are regulated, having that early dialogue can imply the distinction between a clean approval course of and an pointless decline.

Unsure in case your set-up will cross SBA’s key-employee take a look at?

An SBA 7(a) Neighborhood Benefit mortgage officer can stroll you thru your choices.

Listed here are among the commonest questions we hear about SBA mortgage medical director necessities.

How does a medical director have an effect on SBA mortgage eligibility?

If a medical director is important for operations, the SBA would possibly think about them a key administration worker. This might imply they should act as a guarantor for the mortgage.

Does my medical director have to ensure the SBA mortgage?

Generally, sure. It actually depends upon how essential that individual is to the operations and the way the connection is ready up. There are third-party medical director corporations and buildings like Administration Companies Agreements (MSA) or Administration Companies Organizations (MSO) that may assist keep away from naming a selected particular person in your SBA mortgage. It’s a good suggestion to talk with a mortgage officer to grasp what’s wanted.

What’s an MSO/MSA and the way does it assist with SBA compliance?

In easy phrases, an MSO is the enterprise entity that manages the non-clinical facets of the clinic, whereas the doctor oversees the medical aspect. An MSA is a contract utilized by non-physician-owned, regulated wellness companies to meet state licensing and medical oversight necessities. An MSA can present the required medical oversight whereas maintaining enterprise operations separate, which could decrease the SBA’s key-employee dangers that require a medical director to ensure a mortgage.

Completely! Many do, particularly when their enterprise construction correctly addresses the medical director necessities.

Are med spas and IV hydration clinics eligible for SBA loans?

Sure, so long as their licensing, possession, and medical oversight buildings meet SBA expectations.

Having a medical director doesn’t mechanically disqualify a enterprise from SBA financing. However how that relationship is structured issues.

With the appropriate setup, many med spas, IV hydration clinics, well being facilities and wellness companies efficiently use SBA 7(a) Neighborhood Benefit loans to launch and develop. The secret is understanding SBA expectations early and constructing the enterprise construction round them.

Nonetheless planning your clinic? A brief dialog now will help you keep away from structuring points that delay SBA approval later. Join with a Mortgage Officer at present.