{kind=link}

You ditched the 9-to-5 for freedom, flexibility, and the possibility to name your personal pictures. However no one warned you in regards to the first of the month. Hire is due, the web invoice simply hit, and also you’re nonetheless refreshing your inbox ready on three totally different purchasers to pay their invoices. The stress is exhausting. Welcome to the freelance money stream rollercoaster.

Proper now, over 76.4 million Individuals work independently, producing an enormous 1.5 trillion {dollars} yearly. But, nearly all mainstream monetary recommendation assumes you get a neat, predictable direct deposit each two weeks. While you run a contract enterprise, you would possibly pull in $9,000 one month and scrape by on $1,500 the subsequent. Customary monetary guidelines simply don’t work for this actuality.

You want a wholly new system. If you wish to finances irregular earnings with out dropping sleep, you need to construct a framework constructed for the actual world. This playbook cuts the fluff. We’re breaking down precisely how you can stabilize your money stream, deal with taxes with out panic, and pay your self a gentle wage—even when purchasers pay late.

Why Customary Budgeting Recommendation Fails You?

Conventional budgeting frameworks just like the 50/30/20 rule inform you to place 50 p.c of your earnings towards wants, 30 p.c towards needs, and 20 p.c towards financial savings. That recommendation fully breaks down when your earnings drops by 60 p.c throughout a gradual month. In case you tie your spending to mounted percentages of a shifting goal, you’ll always really feel such as you’re failing. The actual enemy right here is the feast or famine cycle.

Throughout a feast month, an enormous fee clears, and all of the sudden upgrading your house workplace feels completely justified. Then the famine hits, leads dry up, and also you scramble simply to cowl fundamental utility payments. With common impartial incomes hitting $108,028 a 12 months for full-timers, this money stream crunch is a common downside. Common workers get predictable deposits and employer-subsidized advantages, however you soak up each monetary shock instantly. You repair this by fully decoupling what your enterprise earns from what your family really spends.

|

Monetary Actuality |

Conventional Worker |

Impartial Freelancer |

|

Pay Timing |

Predictable bi-weekly deposits |

Random, fluctuating funds |

|

Taxes |

Dealt with mechanically by the employer |

Your sole duty to withhold |

|

Time Off |

Paid trip and sick depart |

Zero pay except you saved for it upfront |

|

Advantages |

Sponsored well being & retirement |

100% self-funded overhead |

Price range Irregular Earnings with a Survival Baseline

Overlook fancy spreadsheets for a minute and concentrate on discovering your absolute flooring. You might want to know the naked minimal amount of money required to maintain the lights on, feed your self, and hold your enterprise operational. We name this your Survival Baseline. Pull up your final three months of financial institution statements and spotlight solely the bills you actually can’t ignore. Embody hire, fundamental utilities, grocery store groceries, medical health insurance, and important enterprise software program like internet hosting charges.

Don’t embrace takeout, gymnasium memberships, or streaming providers. Let’s say these core bills complete $3,200. That turns into your magic quantity and dictates your whole monetary sport plan. While you plan your month, your one and solely job is to safe that $3,200 earlier than you spend a single dime on anything. Knowledge reveals 45 p.c of contemporary freelancers use AI instruments to spice up their incomes potential, making it simple to imagine the cash will at all times stream. However dry spells occur, and realizing your actual baseline retains you completely grounded.

|

Expense Class |

What It Consists of |

Precedence Degree |

|

Survival Baseline |

Hire, fundamental meals, house utilities |

Non-negotiable; fund this earlier than anything |

|

Enterprise Ops |

Important software program, quick web |

Should-have to maintain your enterprise incomes |

|

Minimal Debt |

Mortgage minimums, bank cards |

Pay instantly to keep away from harsh penalties |

|

Discretionary |

Consuming out, journey, hobbies |

Minimize solely throughout your gradual months |

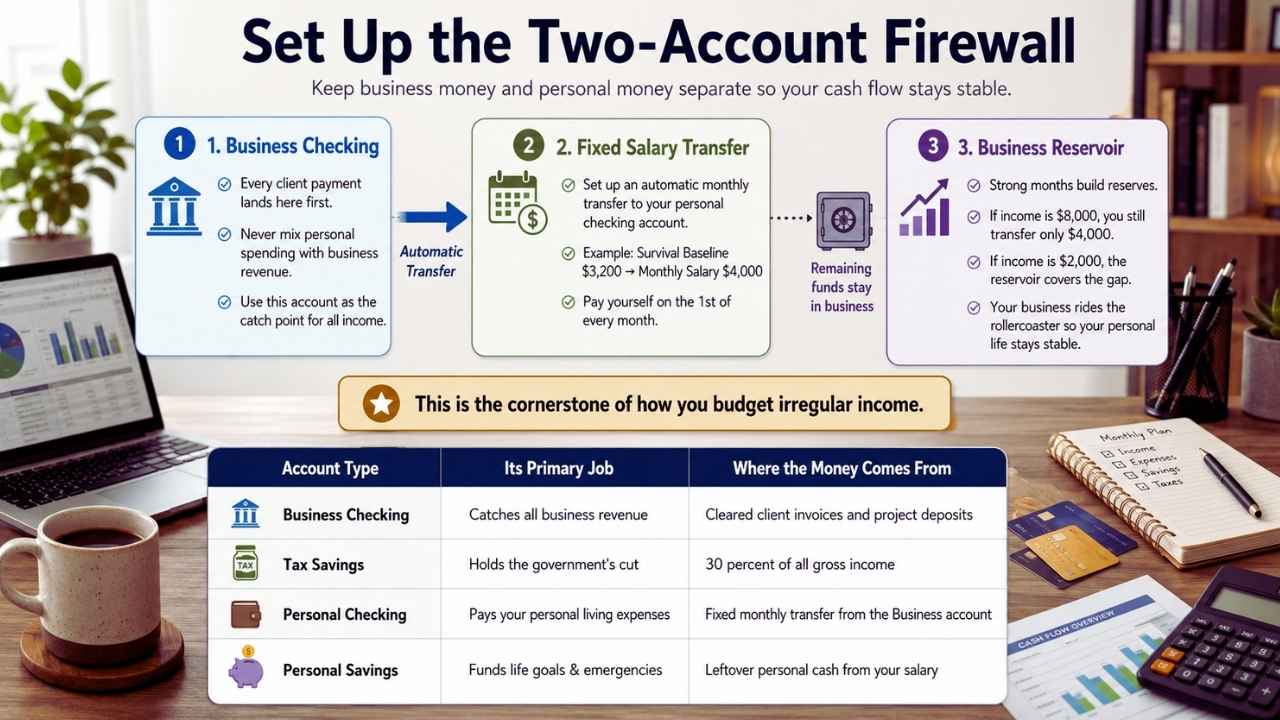

Set Up the Two-Account Firewall

Mixing shopper funds along with your grocery cash creates complete chaos and ensures you’ll mismanage your money. You want a strict monetary firewall, which begins by opening a devoted enterprise checking account at this time. Each single greenback you earn goes into this account first, and also you by no means hand a shopper your private routing quantity. As soon as the enterprise account catches all of the income, you arrange an computerized, recurring switch to your private checking account.

This switch turns into your mounted wage. Begin along with your Survival Baseline plus a tiny buffer for discretionary spending. In case your baseline is $3,200, pay your self $4,000 on the primary of each month. Some months the enterprise brings in $8,000, however you continue to solely switch $4,000. The remaining cash stays behind, constructing an enormous reservoir. When a gradual month hits and also you solely herald $2,000, that reservoir covers the distinction. That is the cornerstone technique while you finances irregular earnings as a result of your enterprise rides the rollercoaster so your private life stays solely steady.

|

Account Kind |

Its Major Job |

The place the Cash Comes From |

|

Enterprise Checking |

Catches all enterprise income |

Cleared shopper invoices and challenge deposits |

|

Tax Financial savings |

Holds the federal government’s reduce |

30 p.c of all gross earnings |

|

Private Checking |

Pays your private residing bills |

Fastened month-to-month switch from the Enterprise account |

|

Private Financial savings |

Funds life objectives & emergencies |

Leftover private money out of your wage |

Tame the Tax Monster

Nothing destroys an impartial enterprise quicker than a shock tax invoice from the federal government. Common workers have their taxes pulled mechanically, however the authorities trusts you to carry their cash till tax season. Break that belief, and the monetary penalties will wipe you out fully. Each time a shopper bill clears, instantly transfer 30 p.c of that cash right into a high-yield financial savings account designated strictly for taxes. Do that earlier than calculating your baseline, earlier than paying your wage, and earlier than shopping for a espresso.

In case you receives a commission $1,000, you need to act such as you solely obtained $700. Monitor your enterprise bills obsessively to decrease your general tax burden, deducting house workplace area, web, and tools prices. In case you function internationally, lean exhausting into native tax-saving instruments. Freelancers in India ought to max out Part 80C investments and fund a Public Provident Fund, whereas US staff ought to leverage a Solo 401(okay) to legally shrink their tax invoice.

|

Tax Motion |

What It Really Takes |

Timing & Execution |

|

Save for Taxes |

30 p.c of each cleared bill |

Instantly upon receiving shopper fee |

|

Pay Estimated Taxes |

Varies closely by location and earnings |

Often quarterly to keep away from authorities penalties |

|

Monitor Deductions |

Log receipts, journey, and software program prices |

Yr-round behavior utilizing accounting software program |

|

Leverage Accounts |

PPF, Part 80C, or Solo 401(okay) |

Yearly to drastically cut back taxable earnings |

Construct Your “Valley” Fund

Mainstream monetary advisors at all times inform you to construct an emergency fund, however impartial staff really need two separate security nets. A private emergency fund handles life’s random disasters, like a blown tire, a damaged tooth, or a leaky roof. A Valley Fund is strictly for your enterprise money stream. Freelance work naturally consists of large hills and deep valleys.

You want money particularly designed to cowl your wage transfers when shopper work dries up or a significant shopper takes 60 days to course of an bill. As you finances irregular earnings to guard your family, this buffer absorbs all of the skilled shock. Purpose to stash two to 3 months of your Survival Baseline instantly inside your enterprise checking account. As soon as that bucket is totally full, you can begin investing your heavy income or reserving lengthy holidays with out an oz. of guilt.

|

Fund Title |

Goal Financial savings Quantity |

When to Really Use It |

|

Valley Fund (Enterprise) |

2 to three months of your baseline |

Consumer dry spells, late invoices, misplaced contracts |

|

Emergency Fund (Private) |

3 to six months of residing prices |

Medical payments, automobile repairs, private disasters |

|

Gear Sinking Fund |

$1,000 to $3,000 money reserve |

Useless laptops, damaged cameras, outdated gear |

|

Tax Holding Fund |

30 p.c of gross income |

Strictly for quarterly and annual tax funds |

Deal with Windfalls Like a Professional

Ultimately, you’ll hit an enormous month the place an enormous challenge closes or three late invoices clear on the very same afternoon. You take a look at your banking app and see an enormous five-figure stability staring again at you. The urge to improve your condominium, purchase a nicer automobile, or splurge on costly workplace furnishings is extremely intense. Don’t contact your life-style. Inflating your baseline due to one nice month is strictly how high-earning freelancers who fail to finances irregular earnings go fully broke.

As a substitute, run that additional money via a strict monetary waterfall. First, pull your 30 p.c for taxes instantly. Subsequent, prime off your Valley Fund so your enterprise buffer is absolutely funded for the subsequent 90 days. Then, wipe out any high-interest bank card debt for an instantaneous return in your cash. Lastly, shove the remaining into index funds or retirement accounts, taking only a small 5 p.c reduce to purchase one thing enjoyable to reward your exhausting work.

|

Precedence |

Motion for Windfall Money |

Why You Should Do It |

|

1 |

Safe the Tax Account |

Prevents large IRS or native tax penalties |

|

2 |

Prime off the Valley Fund |

Ensures subsequent month’s private wage is protected |

|

3 |

Crush unhealthy high-interest debt |

Prompt monetary return in your invested cash |

|

4 |

Make investments & Reward Your self |

Builds long-term wealth and prevents burnout |

Closing Ideas

Monetary mastery doesn’t occur by chance, particularly while you step away from the security of a company payroll. The chaos of a fluctuating paycheck is finally only a math puzzle, and also you clear up it by constructing thick, unshakeable partitions between your enterprise income and your private life. Work out your absolute baseline flooring and cut up up your financial institution accounts at this time.

Pay your self a flat, boring wage, and let your enterprise account take the brutal hits from gradual seasons and late-paying purchasers. While you systematically finances irregular earnings, you fully cease surviving month-to-month and begin constructing actual, generational wealth. It takes critical self-discipline to play the lengthy sport, however the peace of thoughts you achieve is strictly why you turned your personal boss within the first place.

Continuously Requested Questions (FAQs) About Budget Irregular Earnings

Ought to I finances primarily based on my common or lowest month?

All the time finances in your lowest historic month. In case you finances on a mean, you’ll fall brief half the time. Lock in your baseline utilizing your worst-case situation, and deal with every little thing additional as a bonus.

My finest shopper takes 60 days to pay. How do I survive that?

You construct a Valley Fund. If you recognize they function on Internet-60 phrases, depend on your enterprise money buffer to pay your private wage on time. The shopper’s cash ultimately refills the buffer.

How do I deal with large annual payments?

Use sinking funds. If your enterprise insurance coverage is $1,200 a 12 months, divide it by 12. Switch $100 each month right into a sub-account. When the invoice hits, the money is sitting there ready.

What if my baseline is increased than my earnings?

You don’t have a finances downside; you will have an earnings downside. You may’t math your manner out of this. You might want to slash your residing bills, increase your charges at this time, or seize a part-time job to stabilize the ground when you hunt for higher purchasers.