{kind=link}

Key Messages

- The SBA 504 Mortgage Program facilitates long-term, fixed-rate financing for ground-up development, minor/main renovations, tenant enhancements, or buying business/industrial property. This program sometimes requires solely 10 % down, with 40 % funded by an interim lender and 50 % by a standard lender, offering a cheap possibility for increasing companies.

- Approval and funding timelines are influenced by the scope of the work concerned and acquiring thorough documentation. It’s important to accomplice with the lender offering the development/enchancment mortgage to overview website plans, contractor bids, and scopes of labor proper from the start to reduce the necessity for rework on the finish of the venture.

- Carefully monitoring development attracts and alter orders or working with a 3rd social gathering fund management firm are essential for safeguarding interim lenders. They assist be certain that accomplished enhancements are verified, lien waivers are tracked, and prices align with the accepted price range.

- By partnering early with CDC Small Enterprise Finance, lenders can higher handle dangers, anticipate the wants of debtors, and maintain enchancment tasks on schedule from the number of bids, by adjustments within the prices of the venture and timelines to make sure a well timed 504 Debenture takeout throughout the Interim Lenders maturity of their mortgage.

Many debtors trying to buy older or unfinished buildings usually require inside renovations earlier than they’ll begin operations. These renovations are sometimes known as tenant enhancements. SBA 504 financing can help with these upgrades, however solely when they’re made by the borrower within the business property they are going to personal and occupy.. Since these business actual property tasks contain permits, phased development, and a number of draw requests, lenders often search clear steering from the outset.

CDC Small Enterprise Finance, a part of the Momentus Capital branded household of organizations, collaborates with lenders and the small enterprise borrower to confirm venture eligibility, assess timelines, and handle the required documentation all through the venture to make sure a easy and well timed funding..

From the time the lender is structuring the mortgage, finalizing contractor bids and all over closing, early coordination with CDC Small Enterprise Finance helps business actual property debtors perceive what qualifies for eligible SBA financing. Moreover, it supplies lenders with a clearer view of venture timelines, occupancy necessities, and facilitates a easy transition from interim financing to the SBA 504 takeout.

With this stable basis and early partnership, CDC Small Enterprise Finance can establish and assist forestall delays when the scope of the development adjustments throughout development. This permits lenders to help their debtors in making a smoother course of and navigating their development with larger confidence.

Understanding How SBA 504 Tenant Enhancements Work

Understanding how SBA 504 tenant enhancements work is essential for debtors and contractors. The time period tenant enhancements refers to inside renovations completed throughout the area that the borrower will occupy within the bought property. It’s vital to notice that enhancements for third-party tenants don’t qualify.

As Vice President of 504 Mortgage Processing and Closing, I all the time advise that because the borrower should occupy one hundred pc of the improved area, it’s important to establish early on which elements of a constructing are eligible for 504 financing.

Eligible enhancements can embrace HVAC programs, plumbing, electrical upgrades, fireplace and life security enhancements, accessibility modifications, framing, and inside ending work. These enhancements are sometimes obligatory in older buildings or business actual property properties which have had totally different makes use of previously. Moreover, inside enhancements can characterize a good portion of the whole venture price, making early evaluation important.

What can you employ a SBA 504 Tenant Enchancment Mortgage on?

| Eligible Work | Ineligible Work |

|---|---|

| Borrower-Occupied Inside Work Framing, drywall, ceilings, flooring, inside doorways, paint, or insulation |

Enhancements Inside Non-borrower Tenant Suites Beauty upgrades for rental tenants or enhancements benefiting one other enterprise |

| Mechanical & Utility Upgrades HVAC set up or alternative, electrical rewiring, or plumbing upgrades |

Third-Get together Methods Specialty programs for a separate tenant or tools serving a tenant’s unique use |

| Life-Security & Code Compliance Fireplace sprinklers, alarms, ADA upgrades, seismic upgrades, or accessibility work |

Non-Operational Enhancements * Décor, shows, free furnishings, advertising installations or signage not required by code |

| Everlasting Fixtures Constructed-in counters, millwork, fastened casework |

Movable Furnishings * Tables, chairs, décor, detachable shelving |

| Building Attracts (Verified) Progress-based disbursements, site-verified completion, or unconditional lien waivers |

Unverified Attracts Work submitted with lacking documentation or prices that don’t match the accepted scope |

*Non-operational Enhancements and Movable Furnishings aren’t coated except allotted as a Furnishings, Fixtures, and Gear price within the authentic mortgage construction. If a borrower provides them to the scope of labor after mortgage approval, the objects would must be reviewed for eligibility and corrections made to the SBA Phrases and Circumstances. Thus inflicting a possible delay within the funding of the debenture.

Some tasks begin as simple tenant enhancements, however the scope can change as soon as bids are available or partitions come down. When that occurs, the contractor points a change order, which is a proper replace to the scope and price. The interim lender and CDC Small Enterprise Finance will then conduct a re-review utilizing the up to date plans, a revised venture price breakdown (together with sources and makes use of), and all the required permits, invoices, and lien waivers. This ensures that the work remains to be eligible and throughout the construction introduced on the time of SBA approval. If the adjustments are substantial (e.g., they have an effect on eligibility, occupancy, or the accepted price range), underwriting could have to become involved, and a proper mortgage modification will must be issued earlier than the subsequent draw request is accepted.

Work That Might Be Eligible, However Requires Extra Overview

| Doubtlessly Eligible Work | Why It Takes Longer / What’s Wanted |

|---|---|

| Shell Enhancements Supporting Borrower Area Roof restore, exterior structural work, or façade updates tied to borrower use |

Wants up to date plans/website particulars and price allocation so the work is clearly tied to the borrower-occupied portion and isn’t an unique profit to leased-out suites. |

| Specialised Operational Construct-Outs Meals-prep, lab, medical plumbing, or manufacturing or light-industrial areas |

Requires an in depth scope, permits, and documentation displaying the enhancements are everlasting and instantly assist the borrower’s operations. |

| Gentle Prices Architectural and engineering charges, permits, inspections, or affordable contingencies |

Might require further documentation or revisions so prices are affordable, permitted, and totally supported by invoices and lien waivers. |

| Change Orders Affecting Eligibility Modifications shifting work into ineligible areas, proprietor occupancy or the accepted price range |

Typically triggers a overview from underwriting (and generally a mortgage modification) if there is a rise or vital lower to the venture. Overview with the Interim Lender of the proposed change order, revised scope/bids, and an up to date venture price breakdown earlier than further attracts are accepted. |

Understanding the Significance of Occupancy Necessities

SBA 504 occupancy guidelines play a vital function in tenant enchancment tasks. To qualify for an SBA 504 mortgage, debtors have to occupy not less than 51 % of an present constructing or 60 % of latest development. These occupancy ranges dictate which enhancements might be financed.

In the course of the overview course of, the funds can solely be used for the borrower’s portion of the constructing. They’ll enhance the general shell, however debtors can’t enhance the area they’re leasing out to different non-affiliated companies. Since occupancy impacts eligibility, it’s important for business actual property lenders to confirm website plans, proposed scopes, and contractor bids through the preliminary utility section.

Moreover, adjustments to venture scopes can affect eligibility. Important alterations could make it “virtually like a model new mortgage.” Subsequently, early collaboration amongst lenders, CDC Small Enterprise Finance, the contractor, and the borrower is important to keep away from delays. This proactive strategy additionally minimizes rework attributable to change orders that might have an effect on occupancy or the general price range.

Guarantee Your Borrower’s Tenant Enchancment Venture Meets SBA 504 Necessities

Seek the advice of with our SBA 504 specialists to assist your borrower keep on schedule with their enhancements.

How Building Attracts & Fund Management Assist Lenders

Many tenant enchancment tasks require funds to be launched in levels. These are known as development attracts or draw requests. CDC Small Enterprise Finance works with the interim lender all through the development/enchancment course of , and displays the venture’s progress to make sure well timed funding/take out of the Interim Lender Mortgage. This strategy safeguards the lender’s pursuits and helps make sure the interim mortgage is paid off as anticipated, and inside their Interim Mortgage maturity.

Each SBA 504 mortgage requires non permanent funding supplied by the interim lender earlier than the 504 debenture is funded. This interim financing covers the time between real-estate/land closing and venture completion. Lenders stay on this interim place till all development and enhancements are accomplished, mortgage funds are totally disbursed, correct documentation is obtained, and the SBA debenture has been funded.

As soon as the work is accomplished, our inner development workforce will work instantly with the interim lender and the borrower to verify the correct paperwork are so as and meet all native rules and SBA necessities. Moreover, we verify borrower occupancy previous to the SBA mortgage being finalized.

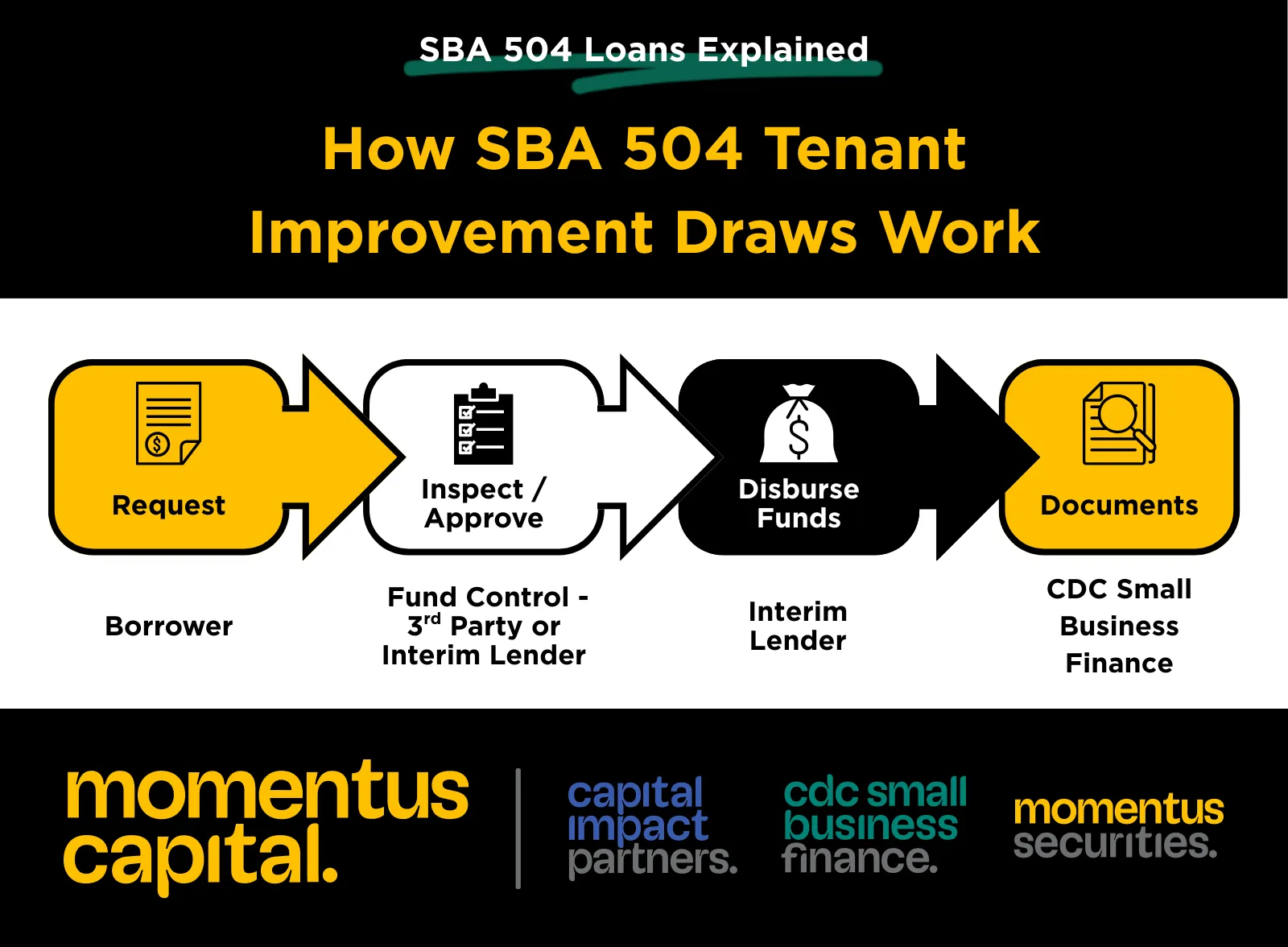

Every draw goes by 4 foremost steps:

- Request: The borrower or contractor submits invoices, schedules, and assist paperwork on to the Interim Lender (Building Mortgage).

- Examine and Approve: The Interim Lender or third Get together Fund management verifies progress, collects lien waivers, and confirms prices align with the accepted scope.

- Disburse: Interim lender releases funds as work is accomplished and often holds onto the ultimate retention till a last signed-off inspection or Certificates of Occupancy is obtained.

- Documentation: CDC Small Enterprise Finance’s inner development workforce works with the Lender and Small Enterprise Borrower to confirm all required documentation meets SBA necessities to be able to proceed with the funding of the debenture.

Lien waivers play an vital function when the SBA 504 debenture funds. These are authorized paperwork from a normal contractor or vendor confirming they’ve been paid for accomplished work and waive any proper to file a mechanic’s lien.

Whereas a lien can nonetheless be filed in some conditions, most frequently by a subcontractor who has not been paid, CDC Small Enterprise Finance advises that any lien waivers which were filed have to be correctly launched to assist guarantee a clear title and funding of the Debenture. Addressing these points early permits the events to resolve disputes in the event that they come up and retains the venture shifting towards last funding with out pointless delays.

We require unconditional lien waivers from the overall contractor or every vendor if a GC was not used. Since tenant enchancment tasks usually contain a number of subcontractors, correct monitoring prevents surprises at closing. This protects in opposition to future claims and ensures a clear title.

Change orders, formal changes to the development contract that change the scope of the venture, can prolong timelines or enhance prices. If a change impacts eligibility or occupancy, lenders ought to anticipate a revised overview and extra documentation. Speaking early might help keep away from delays within the last takeout.

CDC Small Enterprise Finance can start the funding course of to repay the Interim mortgage when:

- Documentation of mortgage proceeds have been totally disbursed and venture prices allotted.

- The venture is one hundred pc full.

- All documentation has been obtained from the municipalities, together with a last, signed-off inspection report (if permits have been required) or a Certificates of Occupancy.

- Unconditional lien waivers are obtained.

Managing Timelines & Interim Financing Publicity

The time it takes to course of business actual property tasks can differ based mostly on allowing, inspections, and last approvals, which frequently results in prolonged venture schedules. Lenders ought to know that some jurisdictions have further necessities that may delay issues by weeks, months, and even years.

Market circumstances and price overruns can affect budgets. Whereas a ten % contingency is often commonplace, current tasks have often gone past that. In such circumstances, the borrower must come out of pocket for the price overruns as SBA solely permits for a ten% contingency to be included within the venture prices. This is the reason CDC Small Enterprise Finance works early on and all through the development/development section to make sure the venture prices stay eligible.

As soon as development is accomplished, last occupancy is accepted by the relevant municipality, and all funds are disbursed, lenders ought to anticipate a 60- to 90-day interval for last funding after the certificates of occupancy is issued. Sustaining clear communication throughout this section might help guarantee a smoother transition to the SBA 504 takeout.

Since interim financing stays in place till all work is completed, lenders profit from clear communication and real looking venture planning. CDC Small Enterprise Finance performs a vital function in setting expectations early, permitting lenders to watch timelines extra successfully.

Why Lenders Work With CDC Small Enterprise Finance

Tenant enchancment and development tasks contain a number of shifting elements. CDC Small Enterprise Finance’s inner assist workforce is a particularly sturdy and educated again workplace. We’re intimately concerned, continually in communication, and managing expectations. This steering helps lenders keep knowledgeable concerning the timeline of the Debenture funding and what the subsequent steps are to start the funding course of for the borrower. ls.

When lenders accomplice early within the mortgage course of with CDC Small Enterprise Finance, they’ll higher anticipate borrower questions, keep away from delays throughout closing, and scale back interim publicity all through the development interval. This steering not solely helps CDC Small Enterprise Finance to remain per last approvals, it permits lenders to know when the interim mortgage is paid off and changed by the everlasting mortgage.

Nonetheless have questions on tenant enchancment eligibility or 504 documentation?

These FAQs cowl the most typical points lenders encounter.

What tenant enhancements/leasehold enhancements are eligible underneath an SBA 504 mortgage?

Eligible enhancements ought to improve the area occupied by the borrower’s enterprise, together with HVAC, electrical, ADA upgrades, plumbing, flooring, and structural modifications. Enhancements made for third-party tenants don’t qualify.

What’s the distinction between tenant enhancements and leasehold enhancements in keeping with SBA pointers?

Whereas these phrases are sometimes used interchangeably, they really check with totally different possession eventualities and eligibility standards. Tenant enhancements usually check with renovations made to a constructing that the borrower owns and occupies, which aligns with the standard construction of an SBA 504 mortgage. Then again, leasehold enhancements sometimes check with upgrades made in an area the borrower is leasing from a landlord.

For SBA 504 functions, financing is tied to the borrower-occupied portion of the property and should instantly profit the working enterprise and meet SBA occupancy necessities. Enhancements supposed for third-party tenants or rented suites don’t qualify for 504 financing.

What documentation is required for tenant enhancements in a 504 venture?

So long as licensing, possession, and medical oversight buildings meet SBA expectations, widespread interim lender necessities embrace: contractor bids, detailed price breakdowns, flooring plans, permits, proof of borrower funding, invoices, lien waivers, and picture/inspection documentation for every draw.

If no fund management was used, invoices and cancelled checks might be required. On the finish of the day, CDC Small Enterprise Finance wants to point out that the mortgage from the lender went to proceeds, the entire cash was disbursed, and present the place the cash was disbursed.

How does fund management work for SBA 504 tenant enhancements?

Fund management entails verifying accomplished work, reviewing invoices, monitoring lien waivers, confirming eligible prices, managing draw requests, and guaranteeing that borrower funds are injected earlier than 504 disbursements.

What occupancy necessities have an effect on tenant enchancment eligibility?

In response to SBA business actual property necessities, debtors should occupy one hundred pc of any area improved with 504 funds and will lease out as much as 49 % of an present constructing and 40 % of latest development. These standards decide tenant enchancment eligibility and shutting necessities.

When ought to lenders interact CDC Small Enterprise Finance for tenant enchancment tasks?

CDC Small Enterprise Finance advises involving them when the lender is structuring their mortgage and earlier than last approval of contractor bids/invoices to make sure that enhancements are eligible, documentation is correct, and interim-lender publicity is minimized.

Subsequent Steps for Lenders

When a borrower is preparing for a tenant enchancment venture, CDC Small Enterprise Finance can help in confirming eligibility earlier than development or enhancements start. This early overview helps keep away from widespread delays and permits lenders to supply clear steering.

Have questions on SBA 504 tenant enchancment eligibility? Contact considered one of our 504 mortgage officers to overview your borrower’s venture earlier than bids or work start.